Planning a trip? Understanding travel insurance exclusions is crucial before you buy a policy. Don’t get caught off guard by unexpected costs. This article delves into the common exclusions found in travel insurance policies, helping you navigate the complexities of coverage and ensure you’re truly protected during your travels. From pre-existing medical conditions to extreme sports activities, we’ll cover the key exclusions you need to be aware of.

Knowing what’s not covered by your travel insurance is as important as knowing what is. By understanding travel insurance exclusions, you can make informed decisions about your coverage options and avoid potential financial burdens should the unexpected occur. This article will empower you to choose the right travel insurance policy and travel with peace of mind, knowing you’re prepared for potential issues.

What Are Policy Exclusions?

Policy exclusions are specific situations, activities, or conditions that are not covered by your travel insurance plan. Understanding these exclusions is crucial before purchasing a policy, as it clarifies what circumstances will invalidate your claim. Ignoring these details can lead to unexpected financial burdens should an unforeseen event occur during your travels.

Essentially, exclusions define the boundaries of coverage. They outline scenarios where the insurance company will not provide reimbursement or assistance. These exclusions are clearly stated in the policy document, and it is your responsibility to review them carefully.

Common examples of exclusions might include pre-existing medical conditions, engaging in extreme sports, traveling against government advisories, or losses resulting from civil unrest. Each policy is unique, so it’s important to analyze the specific exclusions relevant to your chosen plan.

Why Reading the Fine Print Matters

Travel insurance can be a valuable asset when unforeseen circumstances disrupt your trip. However, it’s crucial to understand that policies aren’t one-size-fits-all. They come with specific exclusions that dictate what is and isn’t covered. Failing to read the fine print can lead to unexpected expenses and denied claims, leaving you financially vulnerable.

The fine print outlines the limitations of your coverage. It details the specific scenarios in which the insurance company will not pay out. These exclusions can vary widely between providers and policy types. Common exclusions include pre-existing medical conditions, engaging in extreme sports, travel to high-risk destinations, and cancellations due to foreseeable events. Understanding these exclusions beforehand allows you to make informed decisions about your trip and consider supplemental coverage if necessary.

High-Risk Activities Not Covered

Travel insurance policies often exclude coverage for injuries or losses incurred while participating in certain high-risk activities. These activities are generally considered too dangerous for standard coverage.

Extreme sports are frequently excluded. This can include activities like bungee jumping, skydiving, rock climbing, and certain types of skiing or snowboarding off-piste. Motorsports, such as car racing or motocross, are also typically excluded.

Activities involving aviation, other than commercial flights, may also be excluded. This can encompass piloting small aircraft, hang gliding, and parachuting. Participation in any illegal activity will universally void coverage for any related incidents.

It’s crucial to carefully review your policy details to understand the specific exclusions related to high-risk activities. Some policies may offer optional “riders” to add coverage for particular high-risk pursuits, but this often comes at an additional cost.

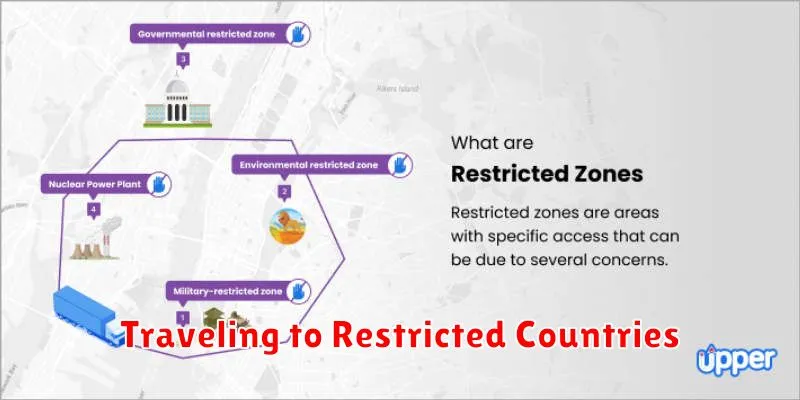

Traveling to Restricted Countries

Traveling to countries against which your government has issued travel warnings or restrictions can significantly impact your travel insurance coverage. Most policies exclude coverage for events related to travel to restricted countries. This is a crucial point to understand when planning international trips.

Before traveling, it is essential to check for any travel advisories issued by your government. These advisories often reflect political instability, safety concerns, or health risks. Ignoring these warnings can invalidate your travel insurance should any issues arise related to the specified restriction.

Insurance providers consider travel to restricted countries a high-risk activity. Therefore, they typically exclude coverage for events such as medical emergencies, trip cancellations, or lost luggage if they occur in a restricted country. Always review your policy wording carefully to understand the specific exclusions related to restricted travel destinations.

Pre-Existing Conditions

Pre-existing conditions are medical conditions that existed before you purchased your travel insurance policy. These conditions can range from minor ailments like asthma or allergies to more serious illnesses such as heart disease or cancer. It’s crucial to understand how your travel insurance policy handles pre-existing conditions as they are often a source of claim denials.

Many policies have specific clauses related to pre-existing conditions. Some policies may exclude coverage entirely for any medical expenses related to a pre-existing condition. Other policies may offer coverage under specific circumstances, such as if the condition has been stable for a certain period before your trip. This stability period can vary significantly between insurers.

Some travel insurance providers offer a “pre-existing condition waiver.” This waiver can provide coverage for pre-existing conditions if certain requirements are met. These requirements often include purchasing the insurance policy within a specific timeframe of your initial trip deposit and ensuring the pre-existing condition is stable and controlled.

Unattended Belongings Clause

Travel insurance policies often include an unattended belongings clause. This clause specifies that the insurer will not cover loss or theft of personal belongings left unattended. This means items left in public places, such as in a car, on a beach, or in a restaurant, are generally not covered if they are stolen or damaged.

Understanding the specifics of this clause is crucial. The definition of “unattended” can vary between policies. Some policies may offer limited coverage if the items were within your line of sight, while others strictly exclude anything not physically on your person or secured in a locked container or safe.

Common examples of situations where this clause might apply include leaving luggage unattended in an airport, a purse hanging on the back of a chair in a cafe, or a camera left on a beach towel. Be sure to carefully review your policy wording for precise details on coverage limitations regarding unattended belongings.

Missed Flight Due to Late Arrival

Travel insurance policies often exclude coverage for missed flights caused by the insured’s late arrival at the airport. This means if you miss your flight because you were delayed by traffic, overslept, or underestimated travel time to the airport, your insurance likely won’t cover resulting expenses.

This exclusion is typically clearly stated in the policy’s terms and conditions. Personal responsibility plays a key role here. Insurers expect travelers to allow ample time for unforeseen circumstances and check-in procedures. Therefore, arriving late due to reasons within your control generally invalidates any claim for missed connection or subsequent travel disruptions.

Exceptions may exist for specific situations, such as unforeseen and unavoidable delays due to public transportation failures, documented road closures, or emergency situations. Always check your policy wording carefully for specifics regarding covered reasons for delay and the required supporting documentation.

{kind=link}